○夢んぼ本部

〒496-8014

住所:愛西市町方町大山田61番1

Tel:0567-25-5913

Fax:0567-55-8120

○第2夢んぼ

〒496-8014

住所:愛西市町方町大山田61番1

Tel:0567-28-1070

Fax:0567-28-1070

○ソーシャルセンター夢んぼ

〒490-1304

住所:稲沢市平和町法立十一丁31番地4

Tel:0567-69-5586

Fax:0567-69-5587

○ワークステーション夢んぼ

第2ワークステーション夢んぼ

〒496-8014

住所:愛西市町方町松川70番地1

Tel:0567-55-7456

Fax:0567-55-7458

○ライフステーション夢んぼ

〒496-8014

住所:愛西市町方町大山田62番1

Tel:0567-31-7811

Fax:0567-31-9171

○ハビリテーションセンター夢んぼ

〒496-8014

住所:愛西市町方町大山田86番地

Tel:0567-69-4448

Fax:0567-69-4446

○青空ヘルパーステーション

〒474 0035

住所:大府市江端町二丁目80番地2F

Tel:0562-74-8883

Fax:0562-74-8884

Content

When a company pays a vendor, it will reduce Accounts Payable with a debit amount. As a result, the normal credit balance in Accounts Payable is the amount of vendor invoices that have been recorded but have not yet been paid. The unpaid invoices are sometimes referred to as open invoices. The information in the purchase ledger is aggregated periodically and posted to an account in the general ledger, which is known as a control account. The purchase ledger control account is used to keep from cluttering up the general ledger with the massive amount of information that is typically stored in the purchase ledger. Immediately after posting, the balance in the control account should match the balance in the purchase ledger. Since no detailed transactions are stored in the control account, anyone wanting to research purchase transactions will have to drill down from the control account to the purchase ledger to find them.

Having separate ledgers makes it easier to see how much is owed to or by each business with which the company trades. A trial balance is a list of all the balances in the nominal ledger accounts.

The total invoiced amount is entered against the supplier’s name, together with an analysis or code of the type of supply. For example, an invoice of $500 for printer paper will be analyzed to the general ledger stationery account. In addition, post the total of $500 to the supplier’s account in the subsidiary purchase ledger.

Isobel Phillips has been writing technical documentation, marketing and educational resources since 1980. She also writes on personal development for the website UnleashYourGrowth. Phillips is a qualified accountant, has lectured in accounting, math, English and information technology and holds a Bachelor of Arts honors degree in English from the University of Leeds. If you’re new to university-level study, read our guide on Where to take your learning next, or find out more about the types of qualifications we offer including entry level Access modules, Certificates, and Short Courses. For the side that does not add up to this total, calculate the figure that makes it add up by deducting the smaller from the larger amount.

If the entries are correctly made in the purchase book, and then posted in the purchase account, the degree of occurrence of error will be zero. While the purchase book gives the required details about the purchases, the purchase account provides total purchases made by the firm every month. At the time of preparing final accounts, the purchase account is generally referred, to transfer the balance in the trading account at the end of the financial year. As against, purchase book is not referred for such purposes. The purchase book contains all the relevant information related to the credit purchase of the goods, such as the name of the vendor, quantity, and rate of the goods and total amount. As against, In purchase account, we only mention the concerned account which is to be credited or debited and the respective amount.

A purchase book is a subsidiary book in which the merchandise purchased on credit is recorded. As against, the Purchase account is a part of the chart of accounts, wherein both cash and credit purchases are posted. Purchase Book is a book of original entry, which keeps a record of credit purchases on a day-to-day basis, which is either used as raw material for production, or as stock for resale to customers. While entering the transactions in the purchase book, one must ensure that the credit purchases are of the items in which the firm is dealing.

MCQs have a number of advantages over traditional examination formats. First, they allow the examiner to ask questions on every topic on the syllabus https://quickbooks-payroll.org/ and thus test the candidates range of knowledge. Perhaps more importantly, correction of answers is entirely objective and comparatively easy.

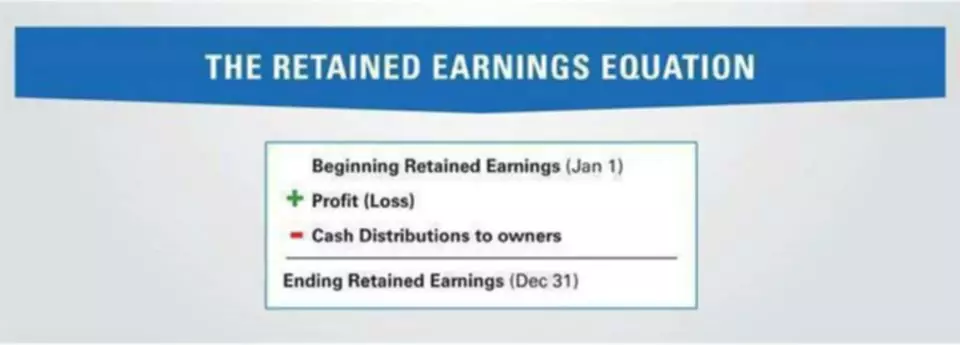

A trial balance is a bookkeeping worksheet in which the balances of all ledgers are compiled into equal debit and credit account column totals. A general ledger acts as a record of all of the accounts in a company and the transactions that take place in them.

Applicability of TDS on it and to check whether TDS is deducted at due rate before making payment or not. Credit balance of the debtors’ account may represent the advance received against the supply of goods; the Auditor should examine and confirm whether any material is supplied against it or not. Periodical statements of creditor should be reconciled.

It helps monitor all the purchases made by the company during the period and ensure that sufficient purchases are made. If there are fewer purchases than required, it will hamper its production process, and on the other side, if there are more purchases than required, it will block the company’s money, which could be used for other purposes. The total amount of the Purchase book, at the end of each month, is taken to the Purchase ledger. Oppositely, the balance of the Purchase Account is transferred to Trading Account, usually at the end of the financial year. One can get the required information relating to credit purchases. When the payment of goods purchased from the seller, is made immediately by the buyer, using cash, card, cheque or via any online mode, it is called cash purchases.

Credits increase liability, revenue, and equity accounts, while debits decrease them. For Example, the following is the purchase journal of the Company How to Balance Purchase Ledger for the period of July-2019. There are no debit and credit sides in Purchase Book, whereas Purchase Account has a debit side and a credit side.

Debits increase asset, expense, and dividend accounts, while credits decrease them. Designed for freelancers and small business owners, Debitoor invoicing software makes it quick and easy to issue professional invoices and manage your business finances. The purchase ledger is also known as the purchase subledger or purchase subaccount. The term ‘stock’ represents the merchandise in which the trader trades, i.e. those items which are bought from the supplier for the purpose of regular sales. Hence, the cloth is a stock for a cloth merchant, diamond is the stock for a diamond merchant. Accounts Payable is also debited when a company returns goods to a vendor or when the vendor grants an allowance.